Cashflow vs Profit: Why Your Business Can Be Profitable and Still Run Out of Cash

Profit is not the same as cash in the bank. Discover why founder-led businesses can be profitable on paper and still struggle to make payroll — and what to track instead.

By Nyasha Madavo, Chartered Accountant & Governance Professional | Capital & Checks

You check your profit and loss statement and it looks great. Revenue is up. Margins are holding. On paper, the business is doing well.

Then you open your bank account.

And wonder where all the money went.

I see this a lot in the founder-led businesses I work with: on paper the business is profitable, but in real life cash is tight because the timing just doesn't line up.

If you have ever felt that disconnect — that unsettling gap between what your financials say and what your bank balance shows — you are not imagining things, and you are not alone. It is one of the most common and least understood financial experiences in founder-led businesses. And it is also one of the most dangerous, because most founders trust the profit number and ignore the warning signs until it is too late.

Here is the truth: profit and cash flow are not the same thing. Understanding the difference is not a finance lesson for finance people. It is a survival skill for every founder.

Why Profitable Businesses Run Out of Cash

This might be the most important sentence in this entire post: 82% of small business failures are caused by cash flow problems — not by a lack of profitability.

That statistic comes from a U.S. Bank study that has been cited extensively across the financial community, and it holds up across markets. Read it again. The majority of businesses that fail are not failing because they are unprofitable. They are failing because they run out of cash while waiting for money that is technically theirs.

That is the trap. And it catches founders who are doing everything right — winning clients, delivering work, growing revenue — because the problem is not performance. The problem is timing.

Profit lives on paper. Cash lives in your bank account.

Profit is calculated using what accountants call accrual accounting. Under this method, revenue is recorded when it is earned — when you complete a project, deliver a product, or issue an invoice — not when the money actually arrives in your account. Expenses are recorded when they are incurred, not when you pay them.

This is useful for understanding the long-term health of a business. But it creates a very specific problem: your profit and loss statement can show a healthy surplus while your bank account is almost empty.

Here is a simple example. Imagine you run a consulting business. In March, you deliver three projects worth $18,000 in total. Your costs for March — salaries, tools, rent — come to $12,000. Your profit and loss statement shows a $6,000 profit for the month.

But your clients all have 60-day payment terms. None of that $18,000 has landed yet. Meanwhile, your salary bill is due at the end of the month, rent is due on the first of April, and your software subscriptions auto-renew now.

Your P&L says you made money. Your bank account disagrees.

The Four Most Common Reasons the Gap Appears

Understanding why profit and cash diverge helps you spot the problem before it becomes a crisis. There are four patterns that come up again and again in founder-led businesses.

1. Late-paying clients and long payment terms

This is the most common culprit. You do the work, send the invoice, and wait. In the US, 56% of small businesses currently have unpaid invoices, with each business owed an average of $17,500 in outstanding payments. In the UK, the picture is even more stark: 90% of businesses experienced late payments in 2025, with the average delay now standing at 32 days — and that is on top of whatever payment terms were agreed. Late payments are now estimated to cost the UK economy nearly £11 billion a year, affecting over 1.5 million businesses and contributing to approximately 14,000 business closures annually.

Every day that money sits unpaid is a day you are effectively lending your client cash — interest free — while still covering your own costs. The gap between effort and payment is where the pressure builds.

2. Growth that outruns cash — overtrading

This one catches founders off guard because it happens precisely when things seem to be going well. You land a big contract, hire to fulfil it, buy the stock or equipment you need, and then discover that the client only pays in 90 days. Your costs are real and immediate. Your revenue is real but delayed.

This is called overtrading — when growth accelerates faster than the cash needed to sustain it. One entrepreneur described it well: "One of the toughest years my company had was when we doubled sales and almost went broke. We were building things two months in advance and getting the money from sales six months late." A business can be winning on every commercial measure and still hit a wall because it does not have the working capital to bridge the gap between spending and receiving.

3. Large upfront costs that show up slowly in your accounts

When you buy equipment, invest in stock, or make a large capital purchase, the full cash goes out immediately. But your profit and loss statement only reflects a small portion of that cost each month, spread over the useful life of the asset through depreciation.

This means your profit can look strong while a significant cash outflow has already happened. The money is gone. The P&L barely shows it.

4. Owner withdrawals and tax obligations

Founder-led businesses are particularly vulnerable here. Profits that look available on paper are sometimes spent before their tax and compliance obligations are fully calculated. Quarterly estimated tax payments in the US, and VAT and corporation tax obligations in the UK, can arrive as jarring cash demands if they have not been set aside throughout the year. An owner drawing from the business ahead of confirmed profit compounds the problem further.

The Difference Your Financial Statements Are Actually Telling You

There are two reports that every founder should understand and use together — not just one in isolation.

The Profit and Loss (P&L) statement answers: Is this business model working? Are we making more than we spend over time? It is the long-view lens. It tells you whether the business is viable.

The Cash Flow Statement answers: Where did the money actually go? Do we have enough cash to operate right now? It is the short-view survival lens. It tells you whether the business can pay its bills.

Profitable businesses that fail do so because their founders watch the P&L closely and ignore the cash flow statement entirely. The P&L flatters. The cash flow statement tells the truth about your week, your month, and your ability to make payroll.

What You Can Do About It — Five Practical Moves

The good news is that most cash flow problems are manageable if you see them coming. The businesses that get into serious trouble are almost always the ones that got surprised. Here is where to start.

1. Invoice immediately and follow up relentlessly

Every day you delay sending an invoice is another day you extend your client's payment window. Invoice the moment work is delivered and ensure invoices sent meet customer invoicing requirements to prevent invoices being rejected for payment. Use software that sends automated payment reminders at 7, 14, and 30 days. Small businesses that use integrated payment tools on their invoices get paid an average of 15 days faster than those that do not. It may feel uncomfortable to follow up, but it is your money.

2. Tighten your payment terms where you can

Not every client will accept shorter payment terms, but many will — especially if you ask upfront before work begins. Consider offering a small early-payment discount (2–3% for payment within 10 days) to incentivise faster settlement. For new clients, a deposit on project work before you begin is entirely reasonable and increasingly common in professional services.

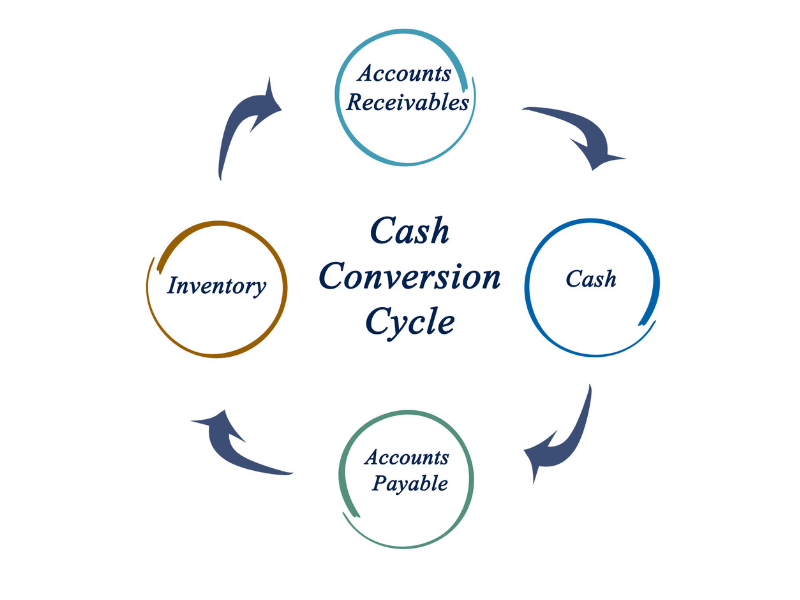

3. Know your cash conversion cycle

This is the time between spending cash (to deliver your product or service) and receiving cash (from the client paying you). The longer that gap, the more cash you need in reserve to bridge it. Understanding your cycle helps you plan ahead rather than react to gaps as they appear. In the US, 55% of invoices are currently overdue, with 33% more than a month late — which means most founders are running a longer conversion cycle than they realise.

4. Run a simple monthly cash flow forecast

A cash flow forecast is not complicated. At its core, it is a month-by-month view of what cash you expect to come in, what cash you expect to go out, and what that leaves in your account. It does not need to be a spreadsheet masterpiece. It needs to be realistic and updated regularly. Research suggests that monthly cash flow forecasting prevents a significant share of cash shortfalls by identifying problems 60 to 90 days before they become critical.

You need to see the problem before it is a crisis — not after.

5. Build a cash reserve and protect it

Service businesses generally need two to three months of operating expenses held in reserve to bridge the gap between when profit is earned and when cash is collected. That number might feel out of reach right now, but even starting to build a buffer — month by month — changes how the business feels to run. Cash reserves are not idle money. They are the difference between making a good decision calmly and making a panicked one under pressure.

The Founder Mindset Shift

The most important shift you can make is this: stop managing your business from your P&L alone and start managing it from your cash position.

Your P&L tells you how the story is going to end. Your cash flow tells you whether you are going to survive long enough to get there.

Both matter. But in the short term — the day-to-day, week-to-week reality of running a founder-led business — cash is the metric that keeps the lights on, pays your team, and gives you the breathing room to make good decisions.[^16]

Founders who understand this distinction do not just avoid the crisis. They build a business that investors, lenders, and partners can trust — because they can explain their numbers clearly, they know where pressure is likely to come from, and they are not surprised by their own bank account.

What to Do Next

If this post made you realise that you have been watching your profit number while your cash flow has been quietly under pressure, that is a useful insight — and an entirely fixable one.

Start with a simple monthly cash flow forecast. Map out what is coming in, what is going out, and what the balance looks like three months from now. Do it this week, before the month gets away from you.

To help you get started, download the free Founder Cash Flow Template below. It gives you a simple, practical structure to track your cash inflows, outflows, and closing balance each month — no finance degree required.

Download the free Founder Cash Flow Template →

Access free cashflow template

And if you want to go further — to make sure your numbers are fully investor-ready and that you understand all five key financial statements your business should be tracking — the Investor-Ready Finance Checklist for Founders covers exactly that.

Get the Investor-Ready Finance Checklist here →

Access finance checklist link

Nyasha Madavo is a Chartered Accountant and Governance Professional, and the founder of Capital & Checks — practical finance and governance content for founder-led businesses.